Informe de fraude Fintech de Veriff: enero a junio de 2020

En nuestro segundo informe de fraude, analizamos el impacto del crimen financiero y el fraude en el mundo de fintech en 2020, y los tipos de fraude más prevalentes observados por Veriff, con datos recopilados de nuestros flujos de verificación.

Patrick Johnson

La industria de la Tecnología Financiera (Fintech) ha ganado impulso a lo largo de los años al transformar la forma en que operan los negocios financieros y proporcionar una amplia gama de servicios a los consumidores. La industria ha evolucionado rápidamente y sigue creciendo. Según el informe 'Oportunidades y Estrategias del Mercado Global Fintech' publicado en julio de 2020:

“El mercado global de Fintech alcanzó un valor de casi US$111,240.50 millones en 2019, habiendo crecido a una tasa de crecimiento anual compuesta (CAGR) del 7.9% desde 2015, y se espera que crezca a un CAGR del 9.2% hasta casi US$158,014.3 millones para 2023. Además, se espera que el mercado crezca a US$191,840.2 millones en 2025 a un CAGR del 10.2% y a US$325,311.8 millones en 2030 a un CAGR del 11.1%.”

Fintech transforma los bancos tradicionales en negocios más rápidos, seguros y coherentes mediante la implementación de tecnologías como Blockchain e IA. Fintech se refiere a cualquier aplicación, software o tecnología que permite a las personas o empresas acceder, gestionar o obtener información sobre sus finanzas o realizar transacciones financieras de forma digital. Posibilitó la realización de operaciones bancarias diarias, comercio, inversión, préstamos, pagos internacionales, etc. a usuarios de todo el mundo. Además, según el informe del Grupo del Banco Mundial, los servicios financieros digitales tienen el potencial de ayudar a los pobres a aumentar sus ingresos y resiliencia al acceder a servicios financieros básicos y banca móvil.

Sin embargo, hemos visto el potencial de fraude y abuso financiero dentro de la industria, con la reciente historia de Wirecard actuando como un recordatorio contundente para los nuevos actores en el mundo financiero sobre la importancia de tener protocolos de gestión de riesgos en su lugar. Pero este fue un fraude a gran escala - ¿qué pasa con los estafadores cotidianos, que intentan robar identidades para obtener acceso a cuentas o ganar beneficios financieros? Esto puede incluir información personal como direcciones, números de teléfono y números de tarjetas de crédito. Esto es lo que Veriff combate diariamente.

Impacto de COVID-19 en Fintech

La pandemia de COVID-19 afectó increíblemente a la mayoría de las industrias. Impactó la estabilidad financiera de las empresas así como de los individuos, enviando a millones a la pobreza. Según las Perspectivas Económicas Globales, se espera que la crisis deje una contracción del 5.2% en la actividad económica global en 2020.

Al mismo tiempo, la crisis trajo una oportunidad para que las empresas Fintech aumentaran su demanda en tiempos de distanciamiento social, cuarentenas y personas adaptándose a una nueva realidad impulsada por la digitalización. La apertura de la tecnología blockchain significa que el lavado de dinero se ha convertido casi en un deporte espectador en algunos rincones de Internet. Hemos escrito en nuestro blog sobre cómo la pandemia impactará el futuro de la industria financiera y las medidas para combatir el financiamiento ilícito.

A medida que muchas empresas buscan volverse digitales, la demanda de procesos de KYC digitales también aumenta. Y aquí es donde Veriff entra, ayudando a otorgar acceso a servicios a usuarios legítimos y bloqueando a los estafadores que acceden a sistemas de gestión de inversiones.

Herramientas de Prevención de Fraude de Veriff

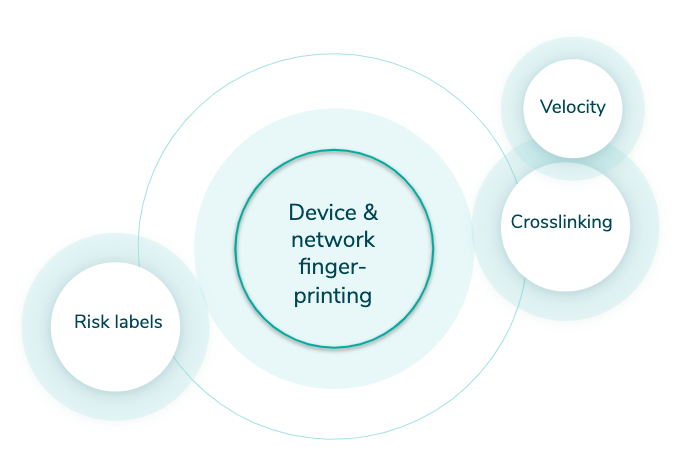

Veriff cuenta con un motor de prevención de fraude desarrollado internamente que automatiza el proceso de toma de decisiones y también asiste a especialistas en caso de que no se pueda hacer una decisión automática (un enfoque híbrido). El motor se puede descomponer en partes más pequeñas, pero todas giran en torno a nuestra solución de huellas digitales de dispositivos patentadas (ver Gráfico 1).

Entrecruzamiento

El cruce de información permite a Veriff agrupar sesiones que comparten puntos de datos similares. Según el conocimiento previo, los estafadores no tienden a limitarse a un solo intento; intentarán verificar hoy, mañana y en los próximos meses y no se detendrán mientras tengan identidades falsas. Toda la información de los cruces se toma en cuenta por nuestro motor de decisiones automático y se reenvía a nuestros clientes.

Gráfico 1. Motor de Prevención de Fraude de Veriff

Abuso de velocidad

El sistema de Velocidad/Abuso asegura que ningún usuario final abusa de su servicio mediante la creación de múltiples cuentas. Teniendo en cuenta toda la información que vemos a través de enlaces cruzados, podemos cerrar automáticamente el acceso a usuarios si ellos, su documento o su dispositivo han sido aprobados anteriormente. Tenemos tres verificaciones de velocidad que se pueden activar todos juntos o de forma independiente:

- Usuario duplicado - verifica si la persona ha sido aprobada anteriormente

- Documento duplicado - verifica si el documento ha sido aprobado anteriormente

- Dispositivo duplicado - verifica si el mismo dispositivo ha sido aprobado anteriormente

Etiquetas de riesgo

Las etiquetas de riesgo señalan los signos de comportamiento fraudulento en las sesiones. Estas etiquetas son utilizadas por nuestros especialistas en revisiones de seguridad más detalladas y se envían a los clientes para darles información sobre la decisión final y ayudar en el análisis posterior.

¿De qué tipos de fraude estamos hablando aquí?

Estamos desglosando el fraude Fintech en 4 tipos principales:

- Fraude documental

- Fraude técnico

- Fraude de identidad

- Fraude recurrente

Analizaremos cada uno en profundidad, qué son, los tipos que vemos más regularmente y el impacto dentro del mundo de la tecnología financiera.

Fraude de documentos

Este es, a menudo, el tipo de fraude de identidad que viene a la mente primero: documentos de identidad alterados o completamente falsos. Estos a menudo existen en forma de identificaciones falsas para una aplicación del mundo real específica: normalmente para acceder a algo para lo que no tienes la edad suficiente, pero en línea, normalmente hay más habilidades requeridas para su creación, y suelen tener un propósito monetario, frecuentemente ofreciendo algún tipo de bonificación financiera por invitar a más usuarios a un sitio.

Así que veamos ambos ejemplos.

Documentos alterados

Existen varios métodos de alteración, pero el resultado final siempre incluye ligeras modificaciones hechas a un documento legítimo con el fin de cambiar parcial o completamente la identidad del titular. Las falsificaciones incluyen, entre otras:

- Alterar o reemplazar la imagen del documento

- Sobre escribir datos del documento con un bolígrafo, lápiz u otras herramientas simples

- Agregar/eliminar datos o elementos específicos del documento

Documentos falsos

Los documentos alterados suelen ser originales falsificados, pero los documentos falsos intentan imitar la apariencia de un documento legítimo pero son reproducciones del original. Estos vienen en forma de:

- Especímenes emitidos por el gobierno alterados que son públicos

- Plantillas prehechas con fotos y datos falsos

En los primeros 6 meses de 2020, el fraude documental representó el 24% de todo el fraude en el mercado fintech (ver Gráfico 2).

Gráfico 2. Fraude documental en fintech

Cómo Veriff enfrenta el fraude de documentos

Nuestra base de datos de documentos interna juega un papel clave en garantizar la precisión de la prevención del fraude documental. La base de datos se actualiza regularmente a medida que realizamos una extensa investigación relacionada con documentos (es decir, encontramos especímenes oficiales, información relacionada con los términos de emisión, etc.) y cooperamos con autoridades gubernamentales de todo el mundo.

Además de nuestra base de datos, el motor de prevención de fraude interno de Veriff juega un papel crucial en la detección y prevención del fraude documental. Con la ayuda del cruce de información, podemos ver si un usuario ha presentado anteriormente documentos alterados o ha estado involucrado en alguna actividad sospechosa.

El fraude documental es el segundo tipo más prevalente de fraude en Fintech, así que, sin importar en qué área se encuentre, estamos listos para ayudarle a abordar este problema. Y créanos, hemos visto diferentes tipos de manipulación de documentos, desde manipulaciones muy obvias de documentos de una sola vez hasta esquemas de fraude complejos, como los siguientes:

“Notamos tráfico inusual proveniente de un país de Europa del Este, asociado con una institución financiera. Lo que generó aún más sospechas fue el hecho de que los clientes estaban presentando documentos emitidos por un país diferente. A primera vista, uno podría pensar que eran personas que estaban viajando, ya que los documentos parecían legítimos y las personas que los presentaban coincidían con la identidad del documento. Pero al tener todos los puntos de datos recopilados por nuestro motor de fraude y la experiencia de nuestros especialistas altamente capacitados, se hizo evidente que los documentos presentados eran falsos y los usuarios finales que los presentaban estaban tramando algo sospechoso. Nuestra investigación posterior reveló que el grupo de estafadores utilizó herramientas desechables para emular tráfico extranjero y crear la ilusión de “legitimidad”, y teníamos razones para creer que el objetivo final de este esquema era preparar a las personas para la migración a un país más desarrollado (con documentos falsos en mano y un historial financiero). Desafortunadamente para estas personas, el viaje fue breve.”

Imagen por Miina Vilo

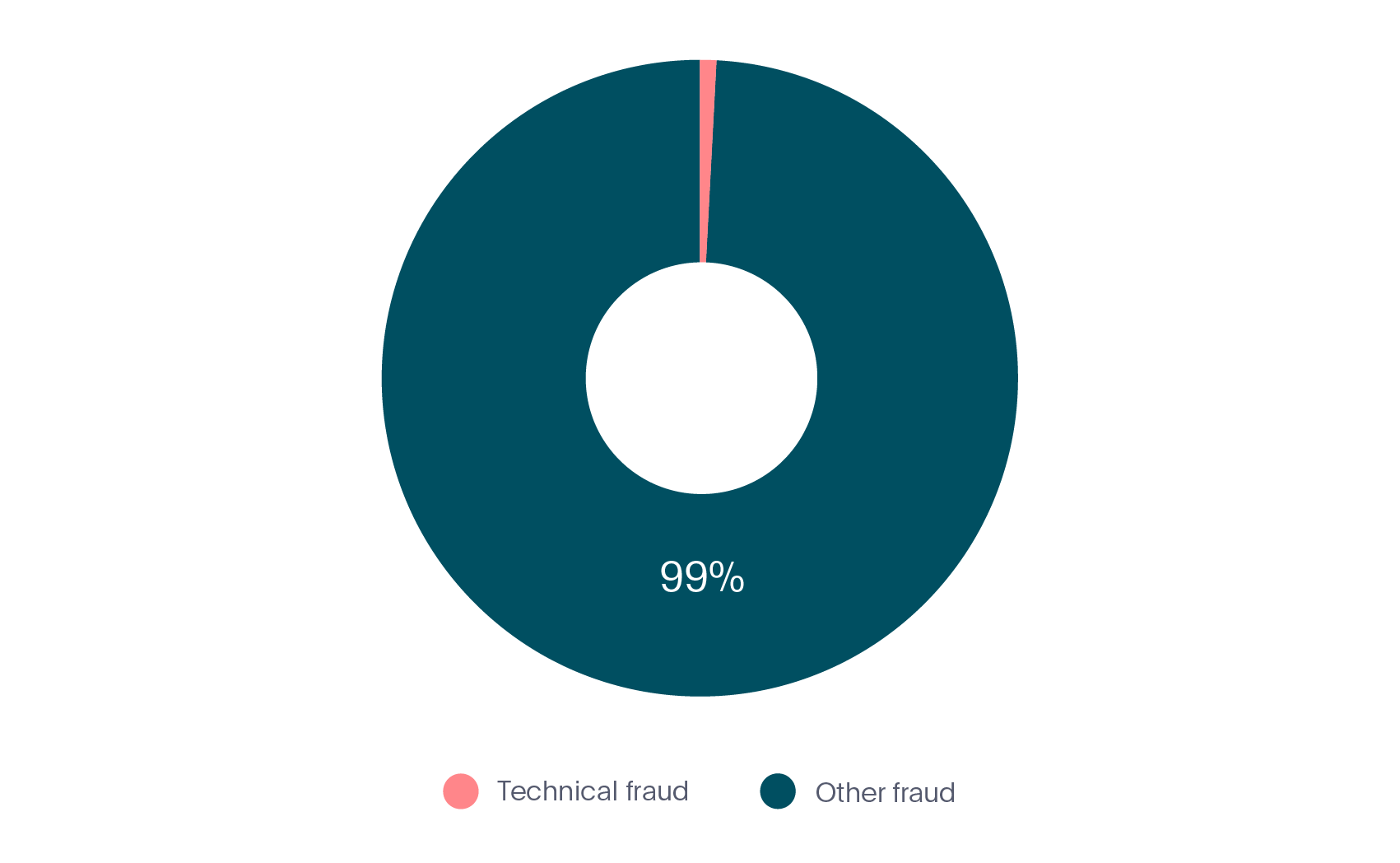

Fraude Técnico

Esto es exactamente lo que podrías esperar, fraude que involucra cierto grado de habilidad técnica que una persona promedio no tendría. En este caso, estamos viendo imágenes transmitidas y acceso fraudulento, dos métodos para aprovechar ofertas y obtener posibles ganancias monetarias.

Imágenes y/o videos se transmiten (o un pase de diapositivas)

Este tipo de fraude ocurre cuando una verificación incluye medios provenientes de una fuente de cámara emulada. Un estafador podría recopilar retratos y fotos de documentos pertenecientes a diferentes personas por adelantado, editarlos en un video y transmitirlo dentro del flujo de Veriff para imitar el proceso en vivo.

Acceso fraudulento a la sesión

Cada vez que un usuario final accede al flujo de verificación, recopilamos información del dispositivo y de la red. Los accesos fraudulentos se definen como:

“Accesos asociados con una sesión de verificación que ha sido accedida desde diferentes redes de países y múltiples dispositivos.”

Este es un indicador de que el enlace de la sesión ha sido compartido fraudulentamente entre diferentes partes.

En los primeros 6 meses de 2020, el fraude técnico representó el 1% de todo el fraude en el mercado fintech (ver Gráfico 3).

Gráfico 3. Fraude técnico en fintech

Cómo Veriff aborda el fraude técnico

Nuestro perfil integral de datos crudos de dispositivos y redes nos brinda control total sobre qué piezas de información utilizamos y en qué contexto. Podemos utilizar elementos específicos de la información del dispositivo para detectar si se usó software de emulación de cámara en algún momento durante el proceso de verificación.

Si detectamos que se utilizó una fuente de cámara emulada para enviar la sesión, lo anotamos, lo que ayuda en la decisión final. También realizamos chequeos en las imágenes de la sesión, para verificar si hay un movimiento natural consistente entre ellas.

Para prevenir posibles accesos fraudulentos en la sesión, buscamos detectar si se está accediendo a una sesión desde diferentes redes de países. Si detectamos un patrón repetitivo que indica acceso fraudulento, automáticamente bloqueamos al usuario con la sospecha de que el enlace de la sesión ha sido comprometido.

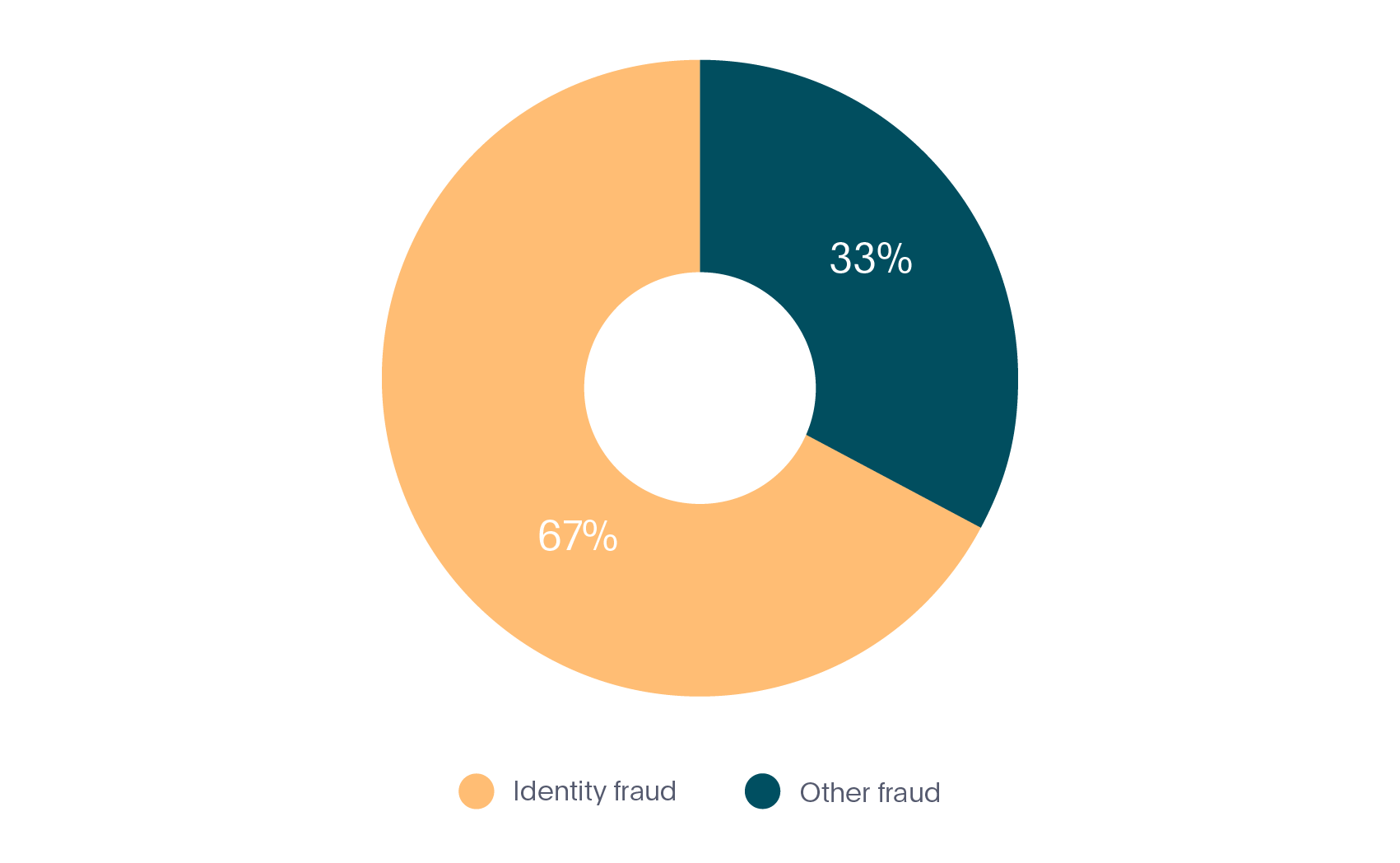

Fraude de Identidad

Ahora llegamos al fraude de identidad. No es muy diferente del fraude documental que mencionamos anteriormente, el fraude de identidad se trata más de la suplantación que de la manipulación real de documentos. Ese es uno de los ejemplos que trataremos de resaltar, de hecho, la suplantación intentada. También veremos la guía de terceros, que implica una presencia más física.

Intento de suplantación

El intento de suplantación es el uso intencional del documento de identidad de otra persona con el objetivo de obtener acceso al servicio en nombre de otra persona. Este tipo de fraude generalmente utiliza un documento físico obtenido ilegalmente de la víctima presentado por un estafador.

Intento de engaño utilizando imágenes falsas

El usuario final no muestra un documento físico real, sino que lo muestra desde una pantalla de dispositivo o en papel impreso mientras utiliza el documento digital de otra persona o un documento manipulado digitalmente.

Guía de terceros

La guía de terceros generalmente involucra asistencia física del usuario final, a veces sin decirles para qué es la verificación. Este comportamiento nos lleva a creer que el usuario final que está siendo asistido no será la persona que realmente utilizará el servicio para el que se están inscribiendo.

En los primeros 6 meses de 2020, el fraude de identidad representó el 67% de todo el fraude en el mercado fintech, convirtiéndose en el tipo más prevalente (ver Gráfico 4).

Gráfico 4. Fraude de identidad en fintech

Cómo Veriff lucha contra el fraude de identidad

Dada la naturaleza de la industria, cada startup de Fintech tiene que mantener un equilibrio entre garantizar el cumplimiento de todas las regulaciones relevantes y ofrecer una gran experiencia al cliente. Y aquí es donde Veriff interviene, con nuestro flujo altamente configurable y sólida prevención del fraude.

Para detectar si se ha iniciado un proceso de verificación con el documento físico de otra persona, comparamos las caras extraídas de un selfie y una foto del documento. Si nuestra confianza en la similitud es demasiado baja, rechazamos la sesión. Si nuestro motor automático no está seguro, destaca los riesgos apropiados y deja la decisión a un especialista.

No es de extrañar que el fraude de identidad sea el tipo de fraude más prominente en fintech. El apetito de actores malintencionados crece junto con la industria, a medida que cada vez más servicios se digitalizan y los clientes ya no tienen que reunirse físicamente con un representante financiero para abrir cuentas o realizar transacciones financieras. Aquí hay otra historia de primera mano desde dentro de Veriff:

“Falsificar una foto en un documento es una cosa, pero falsificar a la persona que presenta el documento es toda otra historia. El villano de esta historia debe haber visto un episodio de “The Office” (la versión estadounidense), donde Dwight Schrute mostró su colección de pelucas para cada persona en la oficina con las palabras: “Nunca sabes cuándo vas a necesitar parecerte a alguien”. Nuestro perpetrador imprimió un documento con una cara bien elaborada y, además, diseñó una máscara que coincidía con la identidad en el documento que estaba mostrando. Si tan solo supiera que pudimos verlo ‘cambiando de cara’, probablemente no habría llegado tan lejos.”

No pierda la oportunidad de explorar las últimas tendencias y obtener asesoría financiera e información práctica esencial para combatir el fraude y proteger su negocio para la inclusión financiera. Descargue nuestro Informe sobre Fraude de Identidad 2024 hoy mismo.

Imagen por Miina Vilo

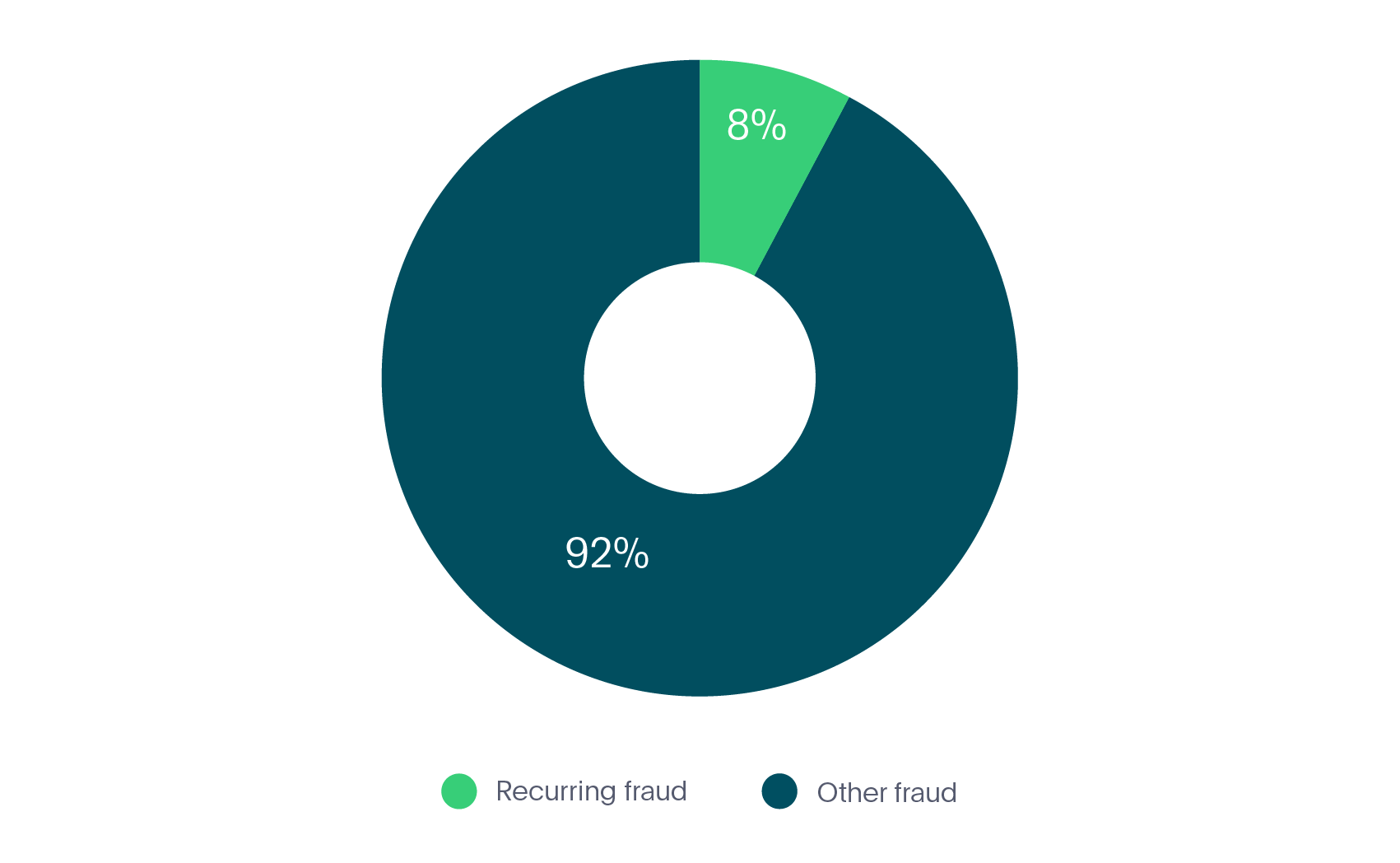

Fraude Recursivo

Finalmente, llegamos al fraude recurrente. Este también se desglosa en dos ejemplos, uno de los cuales es el fraude básico ‘recurrente’, donde un estafador ha tenido éxito y vuelve a intentar. El otro es abuso de velocidad, que explicaremos más adelante.

Recursivo - Fuertes vínculos con fraudes anteriores

Si los estafadores logran abusar del sistema, volverán y lo intentarán de nuevo, si fracasan en hacerlo, volverán y lo intentarán el doble de fuerte.

Abuso de velocidad

El abuso de velocidad funciona de la siguiente manera: después de ser aprobado una vez, los estafadores intentan abusar del sistema y ser aprobados tantas veces como sea posible, lo que generalmente implica verificar a diferentes usuarios reales sin decirles para qué están siendo verificados. Los estafadores suelen llegar a crear identidades sintéticas, donde intentan crear una nueva identidad combinando su información real con datos falsos.

El fraude sintético está encontrando terreno fértil en nuevos tipos de transacciones financieras para consumidores, especialmente con pagos entre pares (P2P).

En los primeros 6 meses de 2020, el fraude recurrente representó el 8% de todo el fraude en el mercado fintech (ver Gráfico 5).

Gráfico 5. Fraude recurrente en fintech

Cómo Veriff lucha contra el fraude recurrente

El fraude recurrente es donde nuestros cruces brillan más. Si estamos seguros de que el usuario final ha cometido fraude antes, rechazaremos automáticamente todos los intentos recurrentes asociados con la misma persona, dispositivo o documento.

Si la misma persona, documento o dispositivo se han encontrado aprobados en las sesiones enviadas anteriormente, todos los intentos recurrentes serán rechazados con Velocidad/Abuso

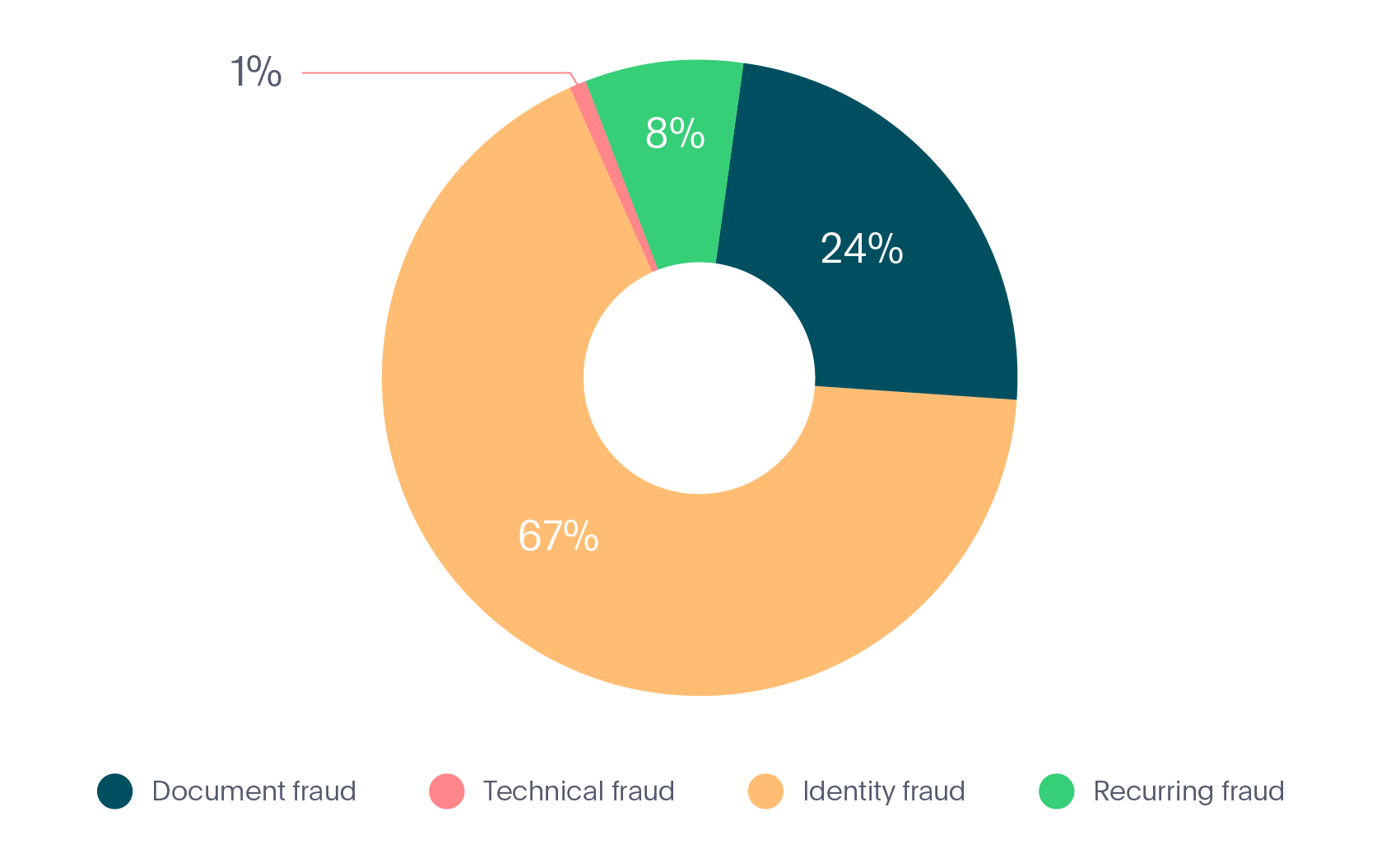

El Desglose General

Ahora que hemos visto los 4 tipos diferentes de fraude que hemos observado dentro de la industria fintech, podemos ver el desglose completo a continuación (ver Gráfico 6):

Gráfico 6. Tipos de fraude en Fintech

- Fraude documental - 24%

- Fraude técnico - 1%

- Fraude de identidad - 67%

- Fraude recurrente - 8%

Por supuesto, en todos los casos anteriores, Veriff está bien posicionado como proveedor de verificación para luchar contra el fraude en línea en todas sus formas. Continuamos observando tendencias en la industria fintech para poder anticiparnos a los desarrollos y prevenir pérdidas para nuestros socios fintech.

Innovaciones Fintech

Las contribuciones de las innovaciones fintech más populares han sido útiles para redefinir las aplicaciones de la tecnología en las finanzas. El área más notable de innovación en fintech apunta a la tecnología regulatoria o RegTech. La innovación fintech encontraría nuevas direcciones de crecimiento en el dominio de la tecnología regulatoria. Aparte de los reguladores financieros, otra innovación es la IA. La inteligencia artificial apoyaría el futuro de fintech y de las empresas que desean utilizar el valor de la tecnología inteligente. La integración de IA como una de las tendencias fintech puede ayudar en la creación de algoritmos sofisticados que puedan examinar perfiles crediticios en pocos segundos.

Si desea aprender más sobre la tecnología de prevención de fraude de Veriff y obtener asesoramiento financiero, puede visitar nuestro sitio web o contactarnos a sales@veriff.com. Y asegúrese de estar atento a nuestro próximo informe que se publicará en un futuro cercano, todo sobre el fraude en Movilidad.