Customer onboarding: quick, secure, and profitable

For unsecured lenders, the need to deliver an optimized customer experience must work alongside the demand to achieve compliance. How can your unsecured lending business prioritize customer experience and security at the same time?

Chris Hooper

If you’re in charge of customer onboarding at your unsecured lending business, then your priorities are clear. Simply put, you want an effective and quick process for new customers, low levels of customer churn and drop-outs, and the best possible customer service that makes people feel welcome and valued.

You know the market is competitive, and that customers often have a broad range of choices, so your baseline priority is to encourage them to pick you. Of course, central to this is the perceived value of your deals, the rate and the terms. But another key aspect is the process of dealing with applications.

You want an effective and quick process for new customers, low levels of customer churn and drop-outs, and the best possible customer service that makes people feel welcome and valued.

Enhancing the customer experience

Applications must be quick, reassuring and secure, otherwise potential customers will head straight to your competitors. They want enough information to feel informed, but not so much that they feel overwhelmed. They appreciate a solid security procedure, but not one that’s onerous and creates needless friction. Plus, they appreciate an interface that’s clear, attractive and speaks to a quality product.

It's perhaps not surprising, then, that 94% of companies see a powerful onboarding strategy as the primary responsibility of the onboarding team, according to a 2023 report by Rocketlane. Meanwhile, in the same study, 78% saw shortening the time-to-value ratio as a vital route to improving experiences.

Customer experience versus security

For unsecured lenders, perhaps as much as any other business vertical, the need to deliver brilliant customer experiences must work in tandem with the requirement to bolster security and comply with a growing set of international regulations, including Know Your Customer (KYC) and those targeting money laundering (AML).

Customers want quick access to approvals, while the regulators (and businesses) want to guard against criminality, particularly fraud.

Sadly, financial crimes are on the rise, driven by digital communications technology, which allows people to carry out thefts and frauds remotely, from anywhere in the world. In the unsecured lending space, a famous example was the estimated £5bn loss suffered by the UK government through its ‘Bounceback’ loan scheme set up to help businesses financially during the Covid pandemic.

Overcoming fraud, improving onboarding

Popular crimes include synthetic ID theft, in which data sets are acquired and used to take out loans. Or online accounts fraud, where passwords are hacked, personal details changed and money taken out.

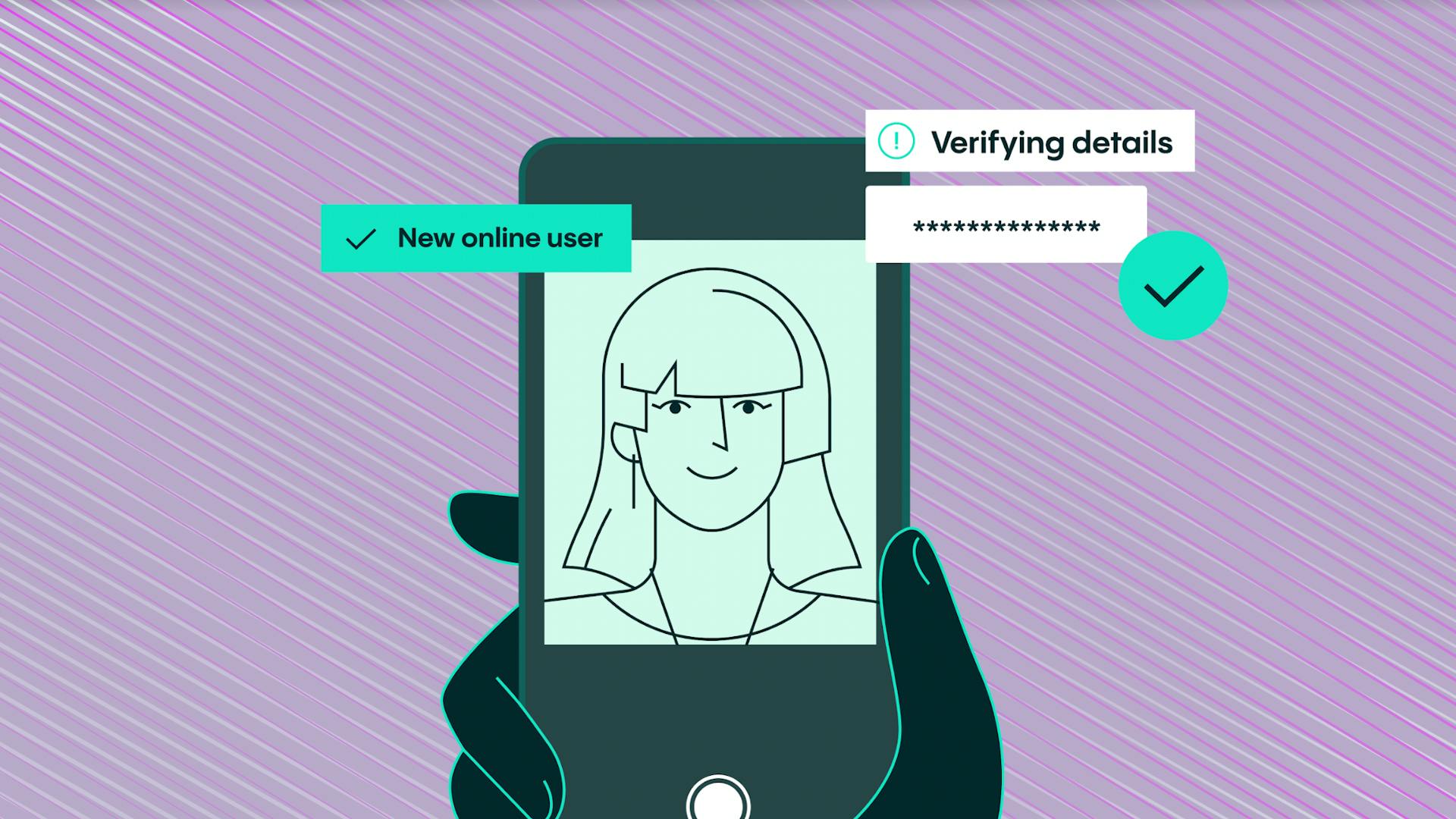

Identity verification tools are a great – and often mandatory – way to combat such challenges. But the process of ensuring a person is who they say they are risks harming conversions, unless it is intuitive, easy and quick.

If your business is looking for an IDV solution, then take your time finding the right tool for you. It should, for example, be able to verify a broad range of government approved documents, ensure the loan applicant is real and that they are the person who is making the application.

It should also fit seamlessly into your onboarding process, reduce friction and optimize time-to-value, while providing enough support to ensure new customers feel like they are being taken care of.

Fast decisions

A 98% check automation rate gets customers through in about 6 seconds.

Simple experience

Real-time end user feedback and fewer steps gets 95% of users through on the first try.

Document coverage

An unmatched 12K+, and growing, government-issued IDs are covered.

More conversions

Up to 30% more customer conversions with superior accuracy and user experience.

Better fraud detection

Veriff’s data-driven fraud detection is consistent, auditable, and reliably detects fraudulent forms of identification.

Scalability embedded

Veriff’s POA can grow with your company’s needs and keep up with times of increased user demand.