What is synthetic identity fraud?

Synthetic identity fraud remains a highly complex and sophisticated crime. It’s attractive for expert fraudsters and crime gangs because criminals receive large payouts and can go completely undetected for a lengthy period of time.

Synthetic identity fraud, which is also sometimes referred to as synthetic identity theft, occurs when a fraudster uses a fake or altered identity in order to fraudulently make an online account, or make a purchase.

To create fake identities, fraudsters usually use a blend of real and fake information. The real information used by a fraudster is often stolen. For example, a photo may be stolen from someone’s Facebook profile. This individual’s social security number or bank account information may either be obtained fraudulently or purchased on the dark web.

Once the fraudster has access to some real information, they will combine this with other pieces of fake information, such as a name, date of birth, or address. When the fraudster has combined the real and the fake information, they can use the newly created synthetic identity to open credit cards or make fraudulent purchases.

A fraudster will first use the new synthetic identity to open an account or conduct another action that will help them build credit, making it seem as though the identity belongs to a real person. Once they’ve built up a credit rating using that identity, they will then either make a large purchase or take out a large loan before they disappear.

Research shows that synthetic identities are more common in the US. This is because identity verification in the US often relies heavily on personally identifiable information (PII) such as social security numbers. As a result, McKinsey estimates that synthetic identity fraud is now the fastest-growing type of financial crime in the country.

Synthetic identity fraud remains a highly complex and sophisticated crime. It’s attractive for expert fraudsters and crime gangs because criminals receive large payouts and can go completely undetected for a lengthy period of time.

Manipulated synthetics vs manufactured synthetics

Although we’ve already outlined how the majority of synthetic identity fraud attacks take place, it’s important to say that there are actually two forms of synthetic identity: manipulated synthetics and manufactured synthetics.

Manipulated synthetics

Manipulated synthetic identities are based on real identities. The identities are considered to be manipulated because limited changes are made to the personally identifiable information associated with the identity, such as the social security number.

An individual may choose to manipulate their identity in order to hide their previous history and gain access to credit. The actions of the individual may also not be malicious. For example, someone with a bad credit history may manipulate their identity in an attempt to gain credit for a legitimate purchase they intend to repay.

Thankfully, manipulated identities are relatively easy for businesses to spot. This is because, as long as you have a piece of software in place that verifies customer identities, it will spot that the manipulated identity collides with the real identity. This means that the identity will not pass a validity check.

Manufactured synthetics

Manufactured synthetic identities previously featured various pieces of authentic data from multiple real identities. Due to this, they were commonly referred to as Frankenstein identities.

However, of late, fraudsters have either used the method we outlined earlier or have built brand new identities entirely from invalid information. In these instances, the personally identifiable information used to create the account does not belong to any known consumer.

How can you prevent synthetic identity fraud?

Synthetic identity fraud is incredibly difficult to detect. This is because victims are typically people who would not regularly access their credit information, such as children, the elderly, or the homeless.

In addition, fraudsters also nurture these identities over time. In doing so, they gradually build their credit score and create a positive payment history. This means that the identity can exist for years and appear incredibly low risk prior to the fraudster maximizing the credit line and disappearing.

Due to the fact that they usually use an element of a real identity, synthetic identities cannot always be spotted by many basic fraud detection tools. But thankfully, there are multiple ways that your business can detect synthetic identity fraud.

For example, your business can make the most of new technologies such as machine learning and artificial intelligence in order to truly understand customer behavior. Once you’ve taken this step, you’ll find it much easier to spot anomalies that could indicate fraud.

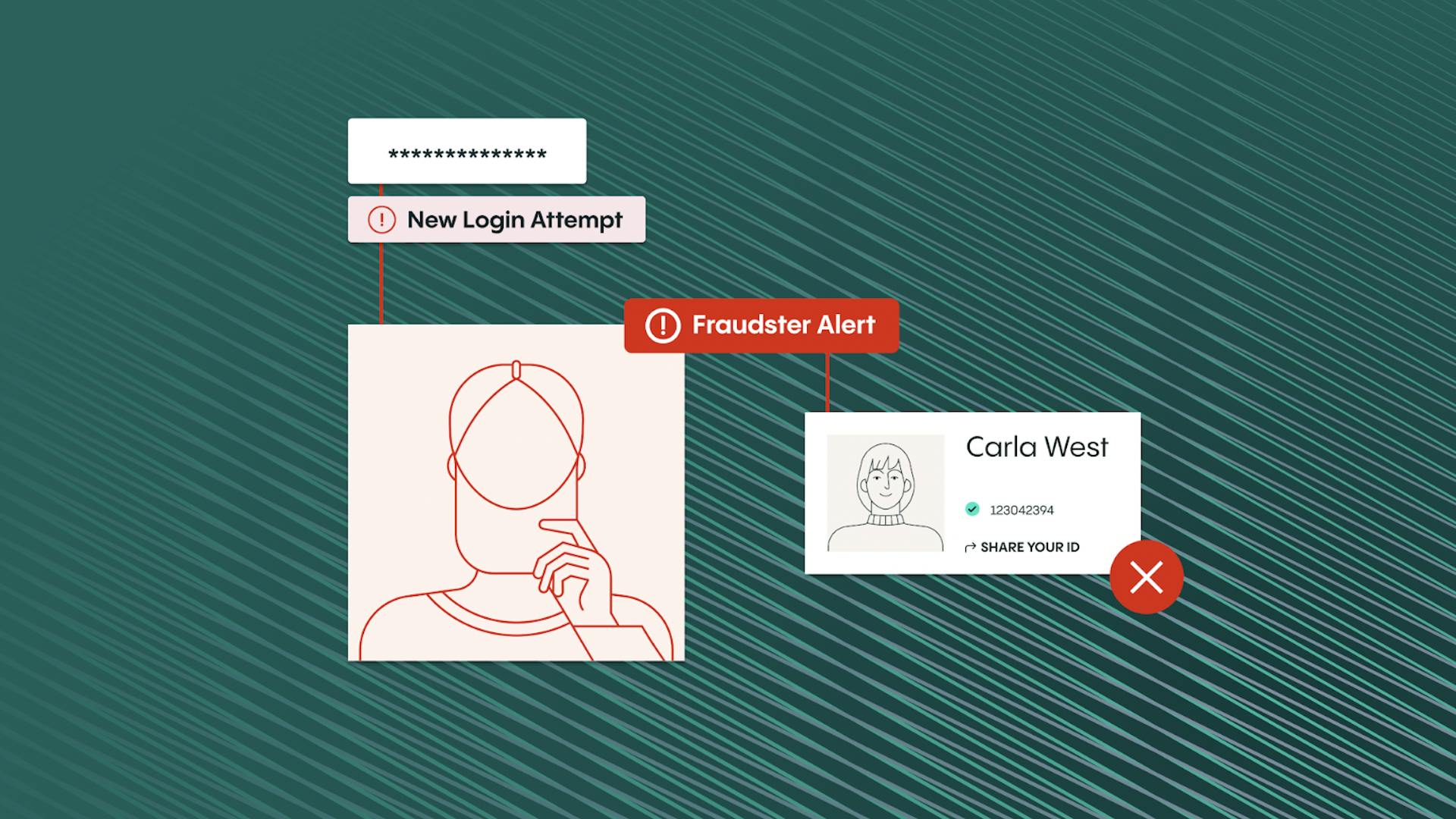

But, the easiest and most comprehensive way of stopping synthetic identity fraud is to employ sophisticated methods of identity verification, such as our ID verification and identity verification solutions. While a synthetic identity can bypass a credit bureau check, it is not sophisticated enough to bypass a document check or an identity check that uses biometric identifiers.

By introducing ID verification processes, your business ensures that a fraudster cannot rely on fabricated information alone. This is because these tools mean that the fraudster needs to submit a fabricated identity document (as they won’t have a genuine identity document that matches the synthetic identity). This fraudulent document will not pass the checks and will be rejected.

Similarly, by employing an identity verification solution that utilizes biometric identifiers, you can stop the fraudster from accessing your services or creating an account. This is because the fraudster will not match the image they’ve stolen for the identity, and they will not want any images of their face to be associated with the fake identity.

So, by employing these systems, you can stop fraudsters in their tracks and ensure that nobody with a fake identity can open an account or access your services.

How to recover from a synthetic identity fraud attack

If your business suffers from a synthetic identity fraud attack, then you should first ensure that the individual can no longer access the account they’ve been using. You should then report the account details to the relevant authorities.

Once you’ve ensured that the synthetic identity cannot be used to exploit your services, you should then review all of your accounts and verify the identities of users. This way, you can identify any other synthetic identities that might be exploiting your services.

Finally, you should then also review your security systems and analyze how this individual managed to bypass them. If you’re reliant on pieces of personally identifiable information such as social security numbers, then you may need to upgrade your security system and instead harness the power of artificial intelligence and biometric identifiers. This way, you can ensure that no other attacks can occur and hurt your business.

How Veriff helps you prevent fraud attacks

Here at Veriff, we’ve created an AI-powered identity verification solution that has been designed specifically to prevent fraud. It can also ensure your customer (KYC) compliance and lead to faster conversions for your valuable customers.

Our solutions make identity verification quick and simple, while also locking out bad actors. User identities are verified in around six seconds and 95% of users are verified on their first try. It reduces fraud by up to 20% and harnesses the power of biometric identifiers to ensure that those who have created a synthetic identity cannot access your accounts or services.

See how Veriff’s fraud prevention solutions can help you - Book a demo

To see how our fraud prevention tools can help keep your business secure, get in touch with our experts today. We’d love to provide you with a free demo that shows exactly how we can help you stop synthetic identity fraud.