Unsecured lending: build security without harming your business

Technology chiefs have enough on their plate without dealing with problematic integrations. Here’s how your unsecured lending business can get better security without losing sales.

Chris Hooper

If you’re responsible for your organization’s technology, then you’ll be only too familiar with the daily challenges this role must overcome. Depending on your job description, you might well have to balance risk, compliance and security with delivering seamless architecture and flawless integrations, all with the executive board breathing down your neck.

In the unsecured lending market, a key part of the global financial services industry, the pressures are as great as anywhere, with the need to keep your tech stack functioning weighed against the scrutiny of financial oversight bodies.

But with today’s fast-changing business landscape comes great opportunities for technology and architecture chiefs to create new paths to profitability for the businesses you run. The digitization of traditionally ‘offline’ businesses gives you the power to optimize processes by leveraging the best tools.

With today’s fast-changing business landscape comes great opportunities for technology and architecture chiefs to create new paths to profitability for the businesses you run.

Solutions that complement your strategy

Key is the ability to create these advantages while ensuring integrations – both proprietary and third-party plug-ins – complement existing infrastructure with neat stack alignment. You might be dealing with legacy infrastructure, or a complicated patchwork of systems that creates inefficiencies and unwelcome risk to operations.

For unsecured lending businesses, failing to conquer these issues risks missing opportunities in a personal loan market worth well over $100bn in the US alone. This is especially important in an era when the value of loans is increasing, by 4.6% in the US between 2020 and 2021.

In short, you need solutions that are simple yet powerful and won’t wreck the smooth functioning of your organization.

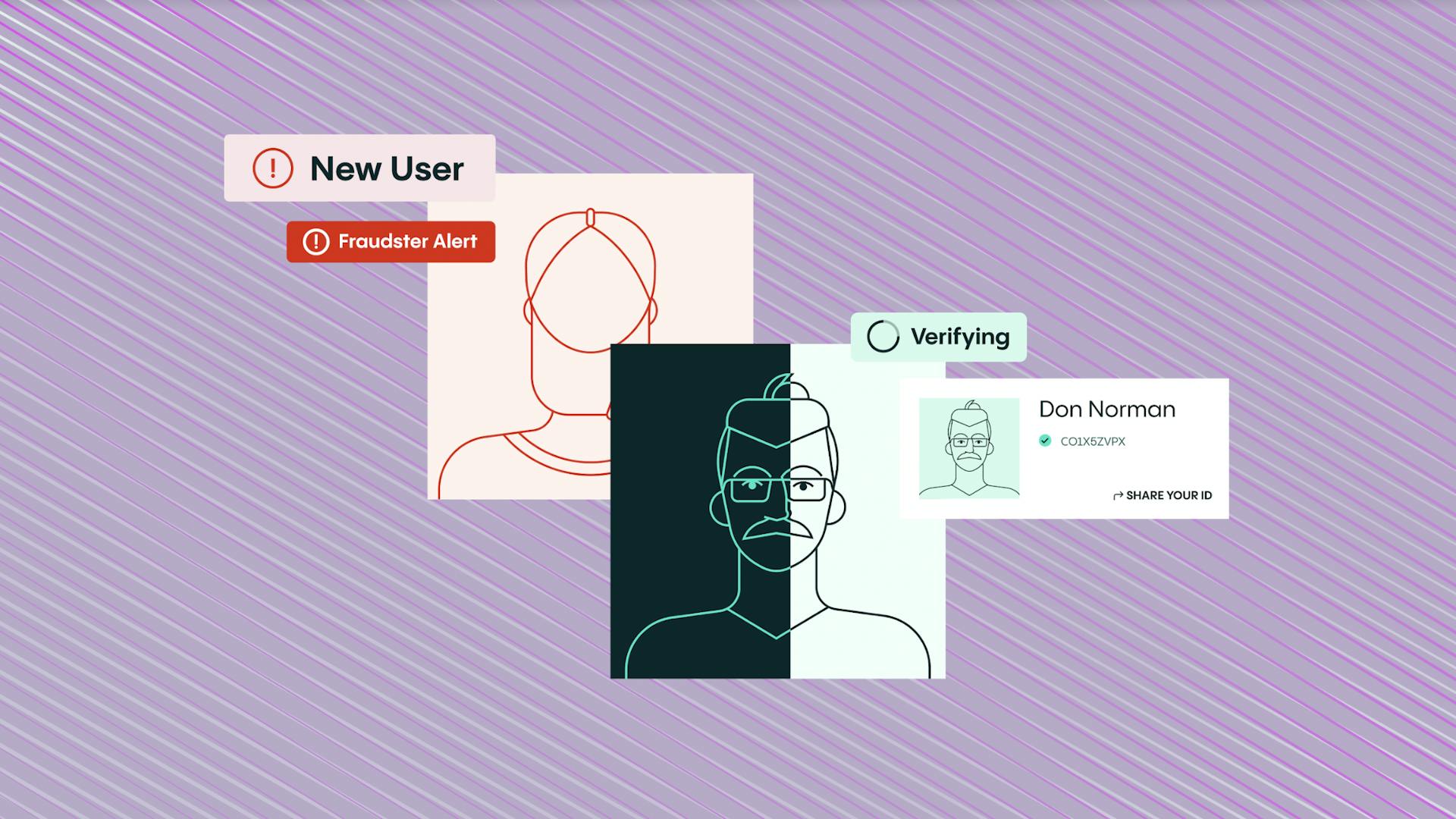

Fighting fraud, but keeping customers on side

One area worth considering is fraud mitigation, responsibility for which is increasingly moving to the IT department. Bad actors are industrious and ingenious, and their reach is global. The problem is growing too, meaning your technology must move with the times.

At time of writing, common scams include synthetic ID theft, where simple data sets are acquired and used to take out loans, or online accounts fraud, in which passwords are compromised, personal details changed and money stolen.

Global regulations, including Know Your Customer (KYC), in most cases make identity verification software a necessity, so you need trusted online tools that don’t get in the way of legitimate loan applications.

Optimizing processes with identity verification

Identity verification (IDV) is a great place to start. There are plenty on the market, so if you’re looking to upgrade, or even considering it for the first time, it pays to research the market.

In a nutshell, a good IDV solution should cover a broad range of government approved IDs, be capable of ensuring the person applying for a loan is the same as the one on the document, and that the identification process is genuine – meaning not faked in some way.

Just as importantly, integration into your existing technology stack should be a doddle, with full alignment and support services on tap. With the right solution, you can ensure comprehensive security without the headache.

Fast decisions

A 98% check automation rate gets customers through in about 6 seconds.

Simple experience

Real-time end user feedback and fewer steps gets 95% of users through on the first try.

Document coverage

An unmatched 12K+, and growing, government-issued IDs are covered.

More conversions

Up to 30% more customer conversions with superior accuracy and user experience.

Better fraud detection

Veriff’s data-driven fraud detection is consistent, auditable, and reliably detects fraudulent forms of identification.

Scalability embedded

Veriff’s POA can grow with your company’s needs and keep up with times of increased user demand.